|

MAIN PAGE

> Back to contents

Finance and Management

Reference:

Kuznetsov N.

Using additive regression models for short-term forecasting of financial macro-indicators and assessing the potential for financing megaprojects

// Finance and Management.

2023. № 2.

P. 15-26.

DOI: 10.25136/2409-7802.2023.2.43657 EDN: TYPVPJ URL: https://en.nbpublish.com/library_read_article.php?id=43657

Using additive regression models for short-term forecasting of financial macro-indicators and assessing the potential for financing megaprojects

Kuznetsov Nikolay

Chief Researcher at the Institute for Economic Policy and Economic Security Problems at Financial University under the Government of the Russian Federation

125167, Russia, Moscow, Leningradsky prosp., 49/2

|

nkuznetsov@outlook.com

|

|

|

Other publications by this author

|

|

|

DOI: 10.25136/2409-7802.2023.2.43657

EDN: TYPVPJ

Received:

28-07-2023

Published:

04-08-2023

Abstract:

The subject of this article is the issue of using additive regression models to predict financial indicators at the macro level. At the same time, special attention is paid to the impact of the economy monetization on the possibility of attracting funding for global development projects (megaprojects). It is shown that the main drawback of the most common forecasting models today is their situation-dependent nature. This, in turn, creates difficulties with the initial setup of the models and the subsequent interpretation of the results obtained, limiting the scope of the models, making the use of this toolkit difficult for financial professionals who do not have special mathematical training. With the help of modeling, forecast values of the gross domestic product (GDP) and money supply (M2) for the short-term time obtained, on the basis of which the expected value of the level of the economy monetization was calculated. Based on a predictive assessment of the level of monetization, it is shown that at the moment the country has a limited potential for increasing domestic debt, which, in the conditions of closing access to international capital markets and partial blocking of state reserves, can become a factor in disrupting the financing of megaprojects for the economy structural modernization. Directions for improving the monetary policy aimed at correcting this situation and increasing domestic investment activity are proposed.

Keywords:

additive regression models, GDP, money supply M2, money-credit policy, short-term forecasting, macro-indicators, megaprojects, economy monetization, structural modernization, financial modeling

This article is automatically translated.

You can find original text of the article here.

Introduction The need to obtain forecast estimates of various financial indicators at the macro level exists today in many areas of activity. Without such forecasts, the state cannot form adequate socio-economic, monetary, fiscal and other policies, and corporations cannot develop strategies for their long-term development, investment and attraction of financing. At the same time, there is still a discussion among professionals about which forecasting method and which predictive model gives the highest quality results (see, for example, the analysis carried out in [1, 2]). However, the majority of experts agree on one thing – financial forecasts are extremely difficult to build. Firstly, because financial processes are characterized by high dynamics and a high degree of uncertainty. Being under the influence of a large number of various factors that simply cannot be fully taken into account within the framework of a mathematical model, they have a difficult-to-predict trend change, cyclical and seasonal effects, as well as significant volatility [3]. And secondly, because the data of financial statistics reflecting these processes, respectively, are characterized by non-linearity, non-stationarity, the presence of outliers and anomalies [4], as well as in some cases omissions in the data and the lack of closure in the series of dynamics, which is due to the peculiarities of the formation and calculation of the corresponding indicators, and repeatedly complicates their synchronization. At the same time, all these features have been further strengthened recently due to the deterioration of the global geopolitical situation. This state of affairs requires the use of modern self-learning models for building financial forecasts, that is, such models that could self-correct in the process of forecasting, adapting to changes in the initial data. Various variants of such models are being developed and used by both Russian [5] and foreign [6] financial institutions. And, nevertheless, research on this issue is still far from being completed and therefore relevant. In this paper, the use of additive regression models for forecasting macro-level financial indicators is considered. As examples, the problem of short-term forecasting of the dynamics of gross domestic product (GDP) and money supply (M2), as well as their subsequent use to assess the level of monetization of the country's economy, as one of the factors determining the potential of the state to attract financing for the implementation of projects of structural modernization of the economy, is considered. Additive regression models for forecasting financial indicators Additive regression models (AR models) are a separate type of statistical models (also related to machine learning methods) based on one-dimensional smoothing of data followed by the construction of nonparametric regression. This approach was first proposed in 1981 [7] and since then has proven to be more flexible and more convenient in comparison with the previously used standard linear regression [8]. According to the AP model approach, the prediction result (each individual element of the set Y, with dimension n) is determined by adding several independent components (see Table 1):

The selection of component parameters is made on the basis of available statistical data using some method known from the literature (for example, a reverse fitting algorithm). Table 1. Key components of the AR model (compiled by the author) | Component | Purpose of the component | | Trend

| Modeling of long-term variable change. To do this, a piecewise linear or logistic function can be used (the latter allows you to simulate growth with saturation, when the rate of its growth decreases with an increase in the indicator). | | Cycle

|

Modeling of long-term fluctuations (waves), such as, for example, economic cycles. The function of a polynomial of the highest degree can be used for this. | | Seasonality

| Modeling of short-term periodically recurring fluctuations typical of the phenomenon of seasonality (weekly or annual). To do this, the method of dummy variables (which take into account repeating patterns in the data), a seasonal function or Fourier series can be used. | | Anomalies

| Responsible for identifying anomalies, including irregular ones, such as, for example, statistical outliers. | | Mistake

| A random component that serves to evaluate information that was not taken into account by previous components (including modeling errors). | Different practical implementations of AR models may have a different set of components (as a rule, less wide in comparison with the one presented above). Overview Several examples of popular AR models used today for making forecasts in the field of finance are given in the table (see Table 2). It can be seen that each of them has both advantages and disadvantages. The choice of a particular model largely depends on the characteristics of the data under study, as well as the goals of forecasting. Table 2. Examples of popular AR models used to predict financial indicators (compiled by the author based on [8]) | Model | Features of use | | Holt-Winters model | The model takes into account trend, seasonality and error to predict time series. Allows you to take into account short-term trends and recurring seasonal factors. It has difficulties with forecasting long-term trends. It is used to predict data with pronounced seasonality and trends, such as, for example, production volumes and product sales. | | The Tail-Vage model | It is a complicated version of the Holt-Winters model, taking into account seasonality and additive trend. It is used to predict indicators in a well-established trend and the presence of seasonal fluctuations. | |

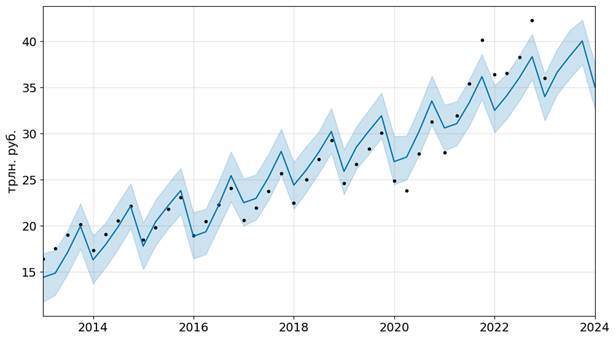

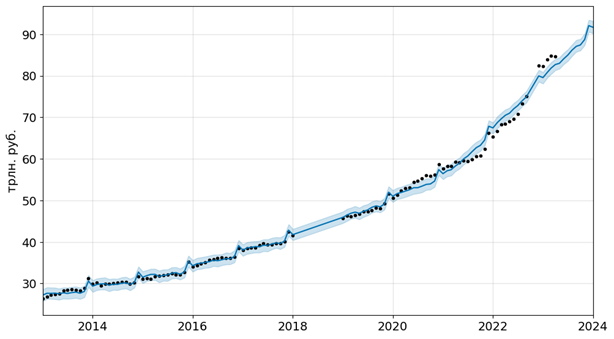

The Freiman-Tukey model | The model takes into account linear and nonlinear trends, seasonal factors and cyclical changes. Adapts well to non-linear dependencies, but requires more complex initial setup. It is used to predict economic indicators when there are complex dependencies and nonlinear trends. | | ARIMA model | The model takes into account autoregression, integration and the moving average in the data. It can be a powerful forecasting tool, but it requires mandatory consideration of the stationarity of the data and the selection of suitable initial parameters of the model. It is used to predict time series with various dependencies and stationarity. | A common disadvantage of all the above models is their situation-dependent nature. To ensure the quality of the received forecasts, their scrupulous initial adjustment is necessary, often achieved only by adjusting, optimizing the initial data or making corrective corrections. In turn, this creates difficulties with the subsequent interpretation of the results obtained. For this reason, their effective use is often inaccessible to specialists in the subject area (financiers, economists) and requires the involvement of specialists in mathematical modeling, data analysis and machine learning. Unfortunately, the latter, in turn, may not have deep knowledge of economics and finance, which allows them to formulate and argue their own conclusions. As a result, this leads to the inability to fully use modeling tools due to the general distrust of the results of the models. In this paper, we used a model from the open source library Prophet, developed for Python and R languages by Facebook's Core Data Science team [9]. The core of the Prophet procedure is implemented in the probabilistic programming language Stan [10] using the principles of Bayesian statistics. According to the tests carried out, this library works well with data series with pronounced seasonal and trend effects, is resistant to data absence and trend shifts, copes well enough with outliers, and in general has a significantly lower error compared to other methods of automatic time series forecasting [11]. From the point of view of practical application, the most important distinguishing quality of the Prophet library is that in order to use it, an analyst does not need a deep knowledge of mathematical methods and predictive modeling, there is no need for a preliminary in-depth study of the initial data series, bringing it to a stationary form, selecting initial approximations and hyperparameters of the algorithm, etc. All this greatly facilitates the use of the model, making it accessible to applied practitioners in the field of economics and finance, and not just mathematicians or analysts. Building short-term forecasts of financial macro indicators using the AR model As an example, let's consider the problem of short-term forecasting of the dynamics of gross domestic product (GDP) and money supply (M2) based on data for the last 10 years (from January 2013 to December 2022 inclusive). The necessary historical data are presented in the reports of the Federal State Statistics Service (Rosstat) "Gross Domestic Product (in current prices)" [12] and "Money supply M2 (national definition)" [13]. It should be noted here at once that these data are presented with different frequency (GDP – quarterly values with an increasing total as of the end of the quarter, M2 – monthly fixed values as of the end of the month), and also that there are no data for February-December 2018 and October-November 2022 in the statistics of the M2 indicator. These circumstances would significantly complicate the construction of a forecast in the case of using any method other than Prophet. Let's make a forecast of GDP and M2 indicators by the end of 2023 (see Figure 1 and Figure 2, respectively).

Figure 1. Forecast of the dynamics of the GDP indicator (calculated by the author)

Figure 2. Forecast of the dynamics of the M2 indicator (calculated by the author) Thus, according to the revised forecast, the possible GDP growth in 2023 (relative to 2022) is unlikely to exceed 3.6% (which will be equivalent to RUB 158.7 trillion). However, at the same time, there is a high probability of near-zero growth or even a drop in GDP by an amount of about -2.9% (that is, up to 148.9 trillion rubles). Thus, even taking into account the crisis situation, our country still has a certain probability of fulfilling the originally laid plans for economic development [14], however, the risks of slipping into recession are also high. At the same time, the value of the average absolute percentage prediction error (MAPE) calculated according to the common methodology for assessing the quality of forecasts [8] was 6.3%, which is a sign of a sufficiently high quality of the constructed forecast.

At the same time, the latest version of the medium-term forecast published by the Bank of Russia at the time of writing [15] presents a significantly narrower forecast corridor, on the one hand assuming a more conservative GDP growth (no more than 2.5%), but at the same time not suggesting its fall at all. This discrepancy can be explained by the fact that the considered forecast model reflects the inertial development, that is, the dynamics of changes in indicators in the conditions of maintaining the existing trends of factor dependencies and the absence of serious financial, external and internal political "disturbances". The forecast of the Bank of Russia also takes into account the likely regulatory impacts, which are not always obvious and obvious to an outsider. At the same time, according to the projected forecast, the volume of money supply will steadily increase. If the current trends continue, by the end of 2023, the value of the M2 monetary aggregate may increase by 19.7%, reaching the value of 84.9 trillion rubles. At the same time, the likely growth spread is from 17.7% to 21.7%. In this case, the value of the average absolute percentage prediction error (MAPE) [8] is 1.5%, which is a sign of a very high quality forecast. Also, the forecast we received almost completely coincides with the medium-term forecast of the Bank of Russia [15], which assumes an increase in the money supply by 17-21%. Assessment of the financing potential of structural modernization projects of the economy Having forecast values of GDP and M2 indicators, it becomes possible to assess one of the most important indicators of the national economy – its monetization coefficient, better known in foreign literature as the "Marshall coefficient" ("Marshallian K") and defined as the ratio of money supply (M2) to gross domestic product (GDP) [16]:

Note that for the correctness of the calculation, it is necessary to use the M2 value averaged over a period similar to the period of calculation of GDP. The monetization coefficient reflects the degree to which the economy is provided with money (that is, its saturation with liquid assets capable of performing the functions of a means of payment) and, in fact, allows linking the financial and real sectors of the economy in a single model. World practice shows that in a market economy, monetization at a level of at least 50% is necessary to ensure the normal operation of economic agents. A decrease in monetization below this threshold leads to a decline in the economy, an increase in barter and offsets due to the lack of a full-fledged possibility of monetary settlements, as well as the growth of the shadow sector of the economy, settlements in which are carried out through alternative financial instruments (for example, cryptocurrencies). To ensure full-fledged investments in fixed assets, the level of monetization of the economy should no longer be lower than 80%. The generally accepted benchmark of monetization for developed countries is the level of 150% [16]. A number of scientists have proved that the high monetization of the economy allows to reduce interest rates on loans and increase their availability [17], increase the liquidity and capitalization of the financial market [18], and, what is especially important in our situation, to stabilize inflation and stimulate economic growth [19]. The latter becomes especially important in view of the ambitious goals outlined by the Government for the modernization and restructuring of the country's economy, the implementation of which is based on large-scale national programs and federal projects (megaprojects) [20]. The table (see Table 3) shows data on the monetization of the economy of various countries for 2020, structured and classified in accordance with the above approach. Table 3. The level of monetization of the economy of some countries (compiled by the author on the basis of [16]) | Monetization level | A country | M2 / GDP | | Tall (more than 150%) | China | 215,6 % | |

Japan | 206,7 % | | Normal (from 80% to 150%) | Great Britain | 133,6 % | | France | 118,0 % | | Germany | 103,0 % | | USA | 91,7 % | | Low (from 50% to 80%) | South AFRICA | 63,2 % | | Russia | 55,0 % | | Brazil | 52,3 % | |

Critical (less than 50%) | Indonesia | 44,7 % | | India | 23,4 % | The level of monetization largely determines the ability of the state to borrow money on the domestic market [21]. It can be seen that our country in 2020 belonged to countries with low monetization of the economy, which indicates a limited opportunity for the country to increase its domestic debt. According to the forecasts of GDP and M2 indicators, the expected level of monetization of the Russian economy in 2023 will increase and may reach 62%. However, in the current economic conditions, due to the closure of access to international capital markets and partial blocking of reserves, this growth may not be enough to ensure full and timely financing of declared national projects and government programs. Thus, it is very likely that the plans announced by the Government of our country for the structural modernization of the national economy will experience a shortage of funding, which may jeopardize the possibility of their implementation on time. On the contrary, an increase in the level of monetization of the economy will contribute to the growth of investment activity within the country and will create the volume of "long money" (that is, long-term investments) needed today, while reducing the cost of lending. Thus, the Central Bank of the Russian Federation and the Ministry of Finance of the Russian Federation today face a difficult compromise task – if the conditions for targeting inflation are met, to ensure targeted regulation of the volume of money supply with bringing the monetization of the economy to the required level. It should be noted here that these tasks have a different horizon – the task of targeting inflation is of a short-term nature (should be solved now), while the task of ensuring sustainable development by saturating the economy with money can be smoothly stretched over time. In this regard, an important role should be assigned to the regulatory function designed to ensure compliance with the targeted nature of the monetary issue and blocking the possibility of liquidity flow to the market of speculative instruments (currency, derivatives, etc.) or to foreign financial markets, and not allowing this money to go into the sphere of final consumption, thereby increasing demand and, accordingly, inflation. One of the possible directions of this could be, for example, the introduction of a segmental reserve ratio, lowered for the industrial sector (to stimulate production growth) and increased for the consumer sector (to contain inflation). Conclusion Thus, additive regression models are an effective tool for forecasting macro-level financial indicators. At the same time, the situation in which our country finds itself today has only increased the value of forecast data, making the speed and ease of obtaining them the key to timely and adequate response to emerging new challenges. The used Prophet library has shown sufficient accuracy, allowing not only to simulate the dynamics of individual indicators (GDP or M2), but also to obtain an indirect assessment of our country's potential for financing its economic development. It is established that despite the possibility of positive economic dynamics, the level of monetization of the economy remains low and may be a hindering factor for the development of the country. This situation obviously goes against the Government's plans to modernize the national economy. In order to correct the situation, it is necessary to continue improving the monetary policy pursued by the state.

References

1. Vertakova, Yu.V. (2016). Review of economic approaches and models for GDP forecasting. Economics and Management, 2(124), 22–29.

2. Abdikeev, N.M., Pashchenko, F.F., Gusev, V.B., Ivanyuk, V.A., Grineva, N.V., Kuznetsov, N.V., Malikova, O.I., & Kuznetsov, V.I. (2019). Modeling the long-term socio-economic development of Russia. Moscow, Russia: KnoRus.

3. Liu, H. & Chan, W.S. (2019). Forecasting the GDP Growth Rate Using Mixed-Frequency Data. International Journal of Forecasting, 35(3), 1002–1015.

4. Matrosov, V.V. & Shalfeev, V.D. (2021). Modeling economic and financial cycles: generation and synchronization. Izvestiya vuzov, Vol. 29, Issue 4, 515–537.

5. Forecasting and model apparatus. Central Bank of the Russian Federation. Retrieved from: http://www.cbr.ru/dkp/system_p/

6. Guide to quarterly national accounts. International Monetary Fund. Retrieved from: https://www.imf.org/external/pubs/ft/qna/pdf/2017/QNAManual2017RUS.pdf

7. Friedman, J.H. & Stuetzle, W. (1981). Projection Pursuit Regression. Journal of the American Statistical Association, 76, 817–823.

8. Lukashin, Yu.P. (20030. Adaptive methods of short-term forecasting of time series. Moscow, Russia.: Finance and statistics.

9. Prophet: Automatic Forecasting Procedure. Retrieved from: https://pypi.org/project/prophet/

10. Stan Development Team. Retrieved from: https://mc-stan.org/

11. Taylor, S.J. & Letham, B. (2017). Forecasting at scale. PeerJ Preprints. Retrieved from: https://peerj.com/preprints/3190/

12. Gross domestic product (quarters). Federal State Statistics Service. Retrieved from: https://rosstat.gov.ru/storage/mediabank/VVP_kvartal_s1995.xlsx

13. Money supply M2 (national definition). Unified Interdepartmental Information and Statistical System. Retrieved from: https://fedstat.ru/indicator/37697

14. Maslennikov, V.V., Sorokin D.E. et al. (2019). Assessment of the forecast of the socio-economic development of the Russian Federation for the period 2019–2024. Finance: theory and practice, Vol. 23, 5, 126–130.

15. Medium-term forecast of the Bank of Russia. Central Bank of the Russian Federation. Retrieved from: http://www.cbr.ru/Collection/Collection/File/45148/forecast_230721.pdf

16. Zenchenko, S., Strielkowski, W., Smutka, L., Vacek, T., Radyukova, Y., & Sutyagin, V. (2022). Monetization of the Economies as a Priority of the New Monetary Policy in the Face of Economic Sanctions. Journal of Risk Financial Management, Vol. 15, 140. Retrieved from: https://www.mdpi.com/1911-8074/15/3/140

17. Goryunov, E.L. (2023). Monetization of the economy: an indicator that shows nothing. Issues of Economics, 3, 126–158.

18. Tosunyan, G.A. (2016). There are reserves for the effective use of the financial system. Bulletin of the Financial University, Vol. 20, 1(91), 8–14.

19. Glazyev, S.Yu. (2019). Dissenting opinion of a member of the National Financial Council on the draft «Guidelines for a unified state monetary policy for 2020 and the period 2021-2022» of the Bank of Russia. Russian Economic Journal, 6, 3–25.

20. Plenary session of the St. Petersburg International Economic Forum. President of Russia. June 16, 2023. Retrieved from: http://kremlin.ru/events/president/news/71445

21. Minakov, A.V. & Lapina, S.B. (2020). Influence of the level of monetization of the national economy on macroeconomic indicators. Russian Economic Bulletin, Vol. 3, 2, 123–130.

Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

Forecasting is an integral element of the management of economic systems. It allows us to determine growth prospects, trends, opportunities and levers of influence on them, which is why economic science pays so much attention to its development. Forecasting financial macro indicators in Russia is carried out not only by the Government and the Central Bank, but also by research centers and the corporate sector, since this direction of forecasting allows us to determine the parameters of market equilibrium and the key ratio for financial activity -"risk-profitability", and therefore assess the prospects for financial results as the ultimate goal of commercial structures. The presented article is devoted to the study of the problems of using additive regression models for short-term forecasting of financial macro indicators. The title of the article generally corresponds to the content. However, let us draw the author's attention to the fact that the title also contains "... and an assessment of the financing potential of megaprojects". At the same time, this aspect is not sufficiently disclosed in the article, only tangentially mentions megaprojects in the text once. Of course, the potential of their financing has not been analyzed and disclosed. We recommend that the author exclude this phrase from the title, or supplement the text of the article with the relevant research results. The article highlights sections with subheadings, which meets the requirements of the journal "Finance and Management". In the "Introduction" the author makes an attempt to substantiate the significance and relevance of the chosen research direction. There are no standard elements for the introduction of scientific articles, such as purpose, objectives, scientific novelty, practical significance, etc. The author needs to supplement the article with these elements. In the section "Additive regression models for forecasting financial macro indicators", the author gives a general description of such models, examines the most popular of them - the Holt-Winters model, the Tail-Wage model, the Freiman-Tukey model, the ARIMA model, as well as methods and applied forecasting tools. The section "Building short-term forecasts of financial macro indicators using the AR model" is devoted directly to describing the results of the author's research on forecasting GDP and the M2 money supply, which are estimated by the author as of 2023 based on Rosstat data. In the section "Assessment of the potential for financing projects of structural modernization of the economy", the author calculates the coefficient of monetization of the Russian economy, compares it with other countries and justifies the conclusion that the existing level of monetization is not sufficient to finance the modernization of the national economy, but the increase in the money supply goes against the policy of inflation targeting of the Bank of Russia. In the "Conclusion" the author records the conclusions based on the results of the study. The research uses both general scientific methods - analysis, synthesis, comparison, ascent from the abstract to the concrete, etc., and special economic methods - correlation and regression analysis, forecasting, modeling, dynamic and coefficient analysis. The relevance of the chosen topic is obvious. Given the turbulence of economic development, the uncertainty of the consequences of sanctions pressure and market restrictions, the issues of economic forecasting in Russia continue to receive even more attention, and especially the development of its methodology. Short-term forecasting of financial macro indicators is in great demand in this regard from both the state and the corporate and private sectors. With the development of technology, forecasting methods are also developing. Today, models based on artificial intelligence and neural network technologies capable of processing large amounts of data are gaining popularity. At the same time, additive regression models do not lose their relevance. The practical significance of the study seems to be high. The results may be of interest to both public authorities and institutional investors. At the same time, the practical significance is not explicitly stated by the author in the article. The author has not formulated the points of scientific novelty of the study. We believe that the elements of increment of scientific knowledge are present in the article, the article should be supplemented with the author's vision of scientific novelty. This will increase the attractiveness of the research for the general readership of the journal. The style of the article is scientific and meets the requirements of the journal. The author actively uses illustrative material, which increases the perception of the research results by readers. The article contains 2 figures and 3 tables. The bibliography is presented by 21 foreign and domestic sources, which does not meet the requirements of the journal. All sources are referenced in the text of the article. The list of sources needs to be expanded. The article failed to develop a scientific debate, there is no literature review as such. At the same time, a comparison of the results of the application of additive regression models by various authors has prospects for the development of scientific discourse. The advantages of the article include the following. Firstly, the relevance and significance of the chosen research area. Secondly, the presence of illustrative material that increases the level of perception of the material by readers. Thirdly, the high quality of interpretation of the results obtained. The disadvantages of the article include the following. Firstly, the absence of explicitly formulated elements of scientific novelty, as well as practical significance. Secondly, the need to adjust the "Introduction" section and supplement it with formalized elements. Thirdly, the need to specify the title of the article. Fourth, the need to expand the bibliographic list in accordance with the requirements of the journal. Conclusion. The presented article is devoted to the study of the problems of using additive regression models for short-term forecasting of financial macro indicators. The article reflects the results of the author's research and may arouse the interest of the readership. The article can be accepted for publication in the journal "Finance and Management" after the elimination of the comments indicated in the text of this review.

Link to this article

You can simply select and copy link from below text field.

|

|