|

MAIN PAGE

> Back to contents

Finance and Management

Reference:

Mamedov M.A., Aliev M.M.

Analysis of the Influence of Financial Technologies on of the Banking Sector of the Russian Economy.

// Finance and Management.

2022. № 4.

P. 1-15.

DOI: 10.25136/2409-7802.2022.4.38887 EDN: PURYHD URL: https://en.nbpublish.com/library_read_article.php?id=38887

Analysis of the Influence of Financial Technologies on of the Banking Sector of the Russian Economy.

Mamedov Murad Azer ogly

ORCID: 0000-0003-2751-8283

PhD in Economics

Department of International Finance, Moscow State Institute of International Relations of the Ministry of Foreign Affairs of Russia (MGIMO of the Ministry of Foreign Affairs of Russia)

119454, Russia, Moscow, Prospekt Vernadskogo, 76

|

murad.mammad15@gmail.com

|

|

|

Other publications by this author

|

|

|

Aliev Magsud Murad Ogly

Postgraduate Student, Department of International Finance, Moscow State Institute of International Relations of the Ministry of Foreign Affairs of Russia (MGIMO of the Ministry of Foreign Affairs of Russia)

76 Vernadsky Avenue, Moscow, 117454, Russia

|

|

maku.aliyev@gmail.com

|

|

|

|

DOI: 10.25136/2409-7802.2022.4.38887

EDN: PURYHD

Received:

05-10-2022

Published:

30-12-2022

Abstract:

The financial sector of the economy, in particular represented by commercial banks, is one of the most progressive. This article analyzes the modern banking sector of the economy, an attempt is made to study the impact of financial technologies on the development and transformation of the banking sector of the Russian economy. To achieve the goals of the study, the authors studied the scientific works of domestic and foreign authors on relevant topics. Based on a review of the literature and an analysis of existing definitions, the author's definition of the concept of financial technology is given, the concepts of fintech and fintech startups are separated. On the basis of statistical data, the authors present data on the volume of fintech transactions, the number of neobanking users, and conduct a macroeconomic content analysis of the level of implementation of financial technologies in the activities of commercial banks. Based on the results of the analysis, the authors came to the conclusion that financial technologies have a significant impact on the development and transformation of both the banking sector of the economy itself and the types of cooperation between commercial banks and fintech startups. At the same time, the level of implementation of financial technologies and the types of interactions between commercial banks and fintech start-ups directly depend on the amount of assets and revenue of commercial banks, and these factors, in turn, influence the determination of the further strategy for the development of commercial banks and their transformation. Given the conditions prevailing in the Russian market, the fintech industry will primarily develop both within the banking sector of the economy and, to a large extent, in cooperation with commercial banks.

Keywords:

financial technologies, fintech, transformation of banks, digitalization, ecosystem, banking ecosystem, digital ecosystem, financial sector, banking sector, banks

This article is automatically translated.

You can find original text of the article here.

Introduction.The financial sector of the economy today, both worldwide and in Russia, can be called one of the most progressive. The banking sector of the economy in Russia, as an integral part and locomotive of the financial sector, on the one hand is one of the largest and most developed, but on the other hand, until recently, the banking business was quite conservative. One of the key factors in the revision of their development strategies by banks and the formation of a new kind of interactions is the development of fintech startups and financial technologies in the financial market in general. There are quite a lot of reasons for the rapid development of fintech companies in recent years. Such reasons include the high customer orientation of such companies, high adaptation to environmental conditions through the use of flexible techniques and new technologies, the use of non-standard tools, etc. The relevance of the research topic lies in the fact that in the conditions of deep digitalization of the financial sector of the economy both worldwide and in Russia, the introduction of innovative technologies into the activities of financial organizations becomes an economic necessity. The introduction of financial technologies is carried out both through the creation of such technologies directly within the banks themselves, and through cooperation with existing companies providing financial technologies. The level of introduction of financial technologies into the activities of banks in this case directly affects the transformation of their business models, including the formation of ecosystems by the largest participants in the financial sector of the economy [11]. The object of research of this article is the financial sector of the economy and commercial banks. The subject of the study is financial technologies and their role in the transformation of commercial banks. The purpose of the study is to determine the level of introduction of financial technologies into the activities of commercial banks and their impact on the transformation of the banking sector of the economy. The scientific novelty of the article is the study of previously unexplored types of interaction between the fintech industry and commercial banks and the determination of the qualitative level of the impact of financial technologies on the transformation of the banking sector of the Russian economy. Despite a large number of separate studies on the topic of financial technologies, digitalization of the financial sector of the economy, models of development of financial and banking organizations, in our opinion, there is no comprehensive analysis of the impact of financial technologies on the transformation of the banking sector of the Russian economy in the scientific literature. The research materials were the scientific works of foreign and Russian authors on relevant topics, which are displayed in the literature review section of this study. The authors also used statistical and analytical data of the Bank of Russia, information, consulting, rating companies and agencies, such as: Deloitte, PwC, E&Y; Association of Banks of Russia, Association of Financial Technologies of Russia, etc. The methodological basis of the research consists of analysis, synthesis, ascent from the abstract to the concrete, logical and historical method, as well as other general scientific methods. Among the specific economic methods, the authors used the analysis of statistical data. Literature review.Before analyzing the impact of financial technologies on the banking sector of the Russian economy, it is worth studying approaches to the definition of the term fintech (financial technologies) and determining its essence. Opinions about the definition of fintech can be divided into two parts: fintech or financial technologies can be defined as a set of innovative technologies in the financial sector of the economy, as well as as a set of organizations providing revolutionary technological financial solutions. R. Alt et al. in their work, they consider fintech as an obvious combination of two applied fields – finance and technology [1]. In this case, the first part of fintech – financial, is considered as a provider of financial services [15]. And the second part is technologies as a way of organizing things, coordinating and simplifying processes [4]. I. D. Kotlyarov defines financial technologies in a narrow sense as a combination of information technologies and financial services or as a combination of innovative financial services with innovative financial technologies [10]. This process is interrelated, since financial technologies generate new financial products, and the created financial products further influence the development of relevant financial technologies [16]. V. V. Maslennikov et al. in their work, they define fintech as a set of young companies providing technologies, software and infrastructure for the provision of financial services [13]. The Financial Stability Board defines fintech as "financial innovations based on the use of technologies that can lead to the creation of new business models, applications, processes or products with a corresponding material impact on financial markets, institutions and the provision of financial services" [17]. In its review, the audit and consulting company Ernst & Young also defines fintech as "organizations that combine innovative business models and technologies to provide financial services, as well as their improvements and significant changes" [19]. It is also worth noting the definition of fintech given by the Central Bank of Russia: "provision of financial services and services using innovative technologies, such as Big Data, artificial intelligence and machine learning, robotics, blockchain, cloud technologies, biometrics, etc." [12]. Within the framework of this study, it is worth separating the concepts of fintech and fintech startup. According to Henner Gimpel et al., "fintech is characterized by the use of digital technologies, such as the Internet, mobile computing and data analytics, to provide financial services, introduce innovations or abandon them. Fintech startups are newly created enterprises offering financial services based on fintech"[6]. The authors also consider it necessary to clarify the definition of the term "ecosystem" used in this study – a set of companies or services and products from different sectors of the economy, united around one organization-platform (in the case of a banking ecosystem – around a banking organization) to more effectively meet the needs of the final recipient and increase their own competitiveness in the market (within a single seamless integrated process) [2].

In this paper, we will adhere to the approach to determining where fintech is a set of innovative technologies in the financial sector of the economy based on the use of innovative and digital means of communication and data processing, transforming both the business models of traditional organizations in the financial market and the interaction between market participants. However, the study will also consider fintech startups as separate organizations providing innovative financial services. Analysis of the fintech market in RussiaIn modern conditions, it is digitalization and the transition of business to online that indicate the rapid development of fintech in the world and in Russia. Figure 1 shows the dynamics of the volume of fintech transactions in Russia in 2017-2021.

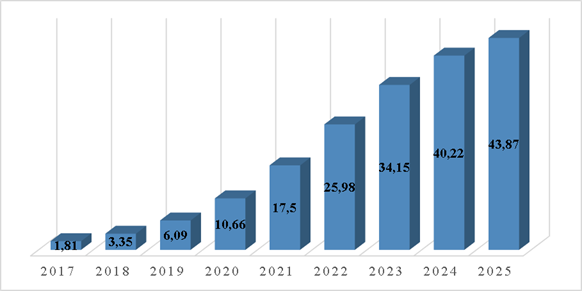

Figure 1. The volume of fintech transactions in Russia in the period from 2017 to 2021 by segment (in millions of US dollars) Source: compiled by the authors according to the report "Fintech in Russia, 2021", Statista In this case, transactions in three main directions were taken as fintech transactions: transactions with electronic payments, transactions in non-banking and transactions related to personal finance. As can be seen from the figure, since 2017, all three directions have shown significant annual growth, and the direction of operations in non-banking has almost tenfold growth. Figure 2 shows the dynamics of the annual indicator of the number of neobanking users in Russia in 2017-2021 and the forecast of development in 2022-2025.

Figure 2. Annual indicator of the number of neobanking users in Russia in 2017-2025. fact and forecast (in millions of people) Source: compiled by the authors according to the report "Fintech in Russia, 2021", Statista. The Russian online services market is growing rapidly, and according to forecasts it can become one of the most developed in the world. According to Statista, the number of users of non-banking banking services in 2017 was 1.81 million people. In just five years, the number of users has grown 17 times to 17.5 million people in 2021. According to forecasts, the number of users will grow rapidly and will be able to reach 43 million people by 2025. The main advantages of neobanking are to quickly meet the needs of customers who seek to minimize time and additional financial costs when interacting with traditional banks. The convenience of banks' platforms in providing online services is gaining more and more users, and there will be more such banks in the future. Digitalization and e-commerce attract more and more consumers to online platforms, and the share of offline store customers is decreasing every year, especially this process began to intensify during the coronavirus pandemic. All these processes directly and actively affect the digitalization of the financial sector of the economy and the development of online banking. Figure 3 shows the dynamics of the degree of penetration of online banking in Russia in the period 2010-2021.

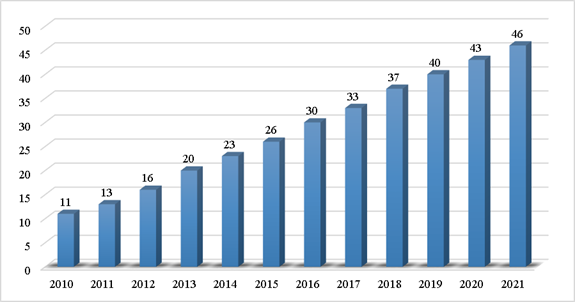

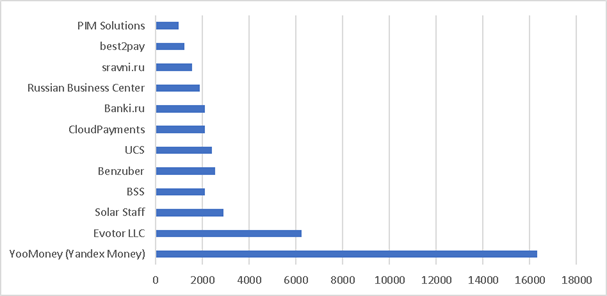

Figure 3. The degree of penetration of online banking in Russia, in 2010-2021. Source: compiled by the author according to the report "Fintech in Russia, 2021", Statista. According to Figure 3, over the past decade, the percentage of online banking penetration in Russia has almost quadrupled - from 11% in 2010 to 46% of the population in 2021. According to the authors, the peculiarity of the Russian fintech industry is the concentration of technological competencies directly in the banking system, which explains why the segment of independent fintech projects (up to 300 companies) is still poorly developed compared to other foreign markets, for example, the USA, Great Britain, Singapore, etc. Banks (for example, Sberbank, VTB, AK Bars, etc.) themselves actively introduce financial technologies, buy promising startups or enter into strategic partnerships, implement acceleration and incubation programs. The key reason for the current situation is the lack of interest of foreign and Russian investors in domestic startups, and traditional players have a powerful resource base. Digitalization of all sectors of the economy, from agriculture to information technology (IT), makes high demands on fintech companies, because the profitability of the business depends on them. Due to the high demand, the fintech sector is developing very quickly and is becoming increasingly competitive. This dynamic is actively supported by the Central Bank of Russia, because thanks to fintech business becomes more transparent. The largest fintech companies in Russia are connected with finance and online payments. Figure 4 shows the 12 largest fintech companies in Russia by revenue in 2020.

Figure 4. The leading fintech companies in Russia in 2020 by revenue (in millions of rubles). Source: report "Digital Services in Russia, 2021", Statista.

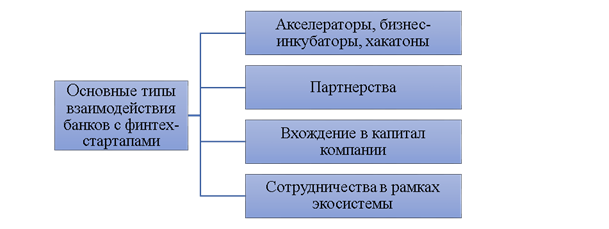

The largest fintech company in Russia by revenue in 2020 became Yumopeu - this is the name given to Yandex.Money" after rebranding and transfer to the ownership of the digital ecosystem of "Sber". The revenue of YUMOPEU in 2020 exceeded 16 billion rubles, which is ten times higher than the revenue of the next largest fintech company in Russia, the leading manufacturer of online cash registers "Evotor LLC". The top ten largest fintech companies in Russia in 2020 also included Solar Staff (a service for automating document flow and payments to freelancers), BSS (a service for remote banking), Benzuber (an online service for paying for fuel at gas stations and refueling using a mobile application), UCS (provides services in the field of payment technologies), "CloudPayments" (online payment acceptance service), "Banki.ru "(financial supermarket), "Sravni.ru " (supermarket of financial and insurance services), "Best2pay" (processing center aggregating payments in the network for large and small companies), "PIM Solutions" (develops services for online stores). The impact of fintech on the activities of commercial banksThe Russian fintech market, unlike foreign ones, can be called quite monopolized, that is, the main trends of the Russian fintech market can be considered a large concentration of financial technology development within the largest banks, as well as to a small extent within telecommunications and IT companies. First of all, this is due to the fact that the financial market in Russia as a whole is quite saturated. Secondly, conditions where a significant part of financial transactions is regulated by the state also play a role. At the end of 2016, the Fintech Association was established, the purpose of which is to develop and implement new technological solutions to ensure the development of the financial market of the Russian Federation and create conditions for the digitalization of the economy. The main activities of the Fintech Association are: remote identification and digital identity management (remote identification, digital profile, technical device analysis service), development of distributed registry technology (masterchain, electronic mortgage accounting, digital bank guarantee, digital letter of credit), development of retail payment space (fast payment system), development of open APIs, legal regulation of surveys on the use of big data technology and electronic interaction with state information systems (general regulation of big data, electronic interaction with state information resources), independent assessment of qualifications in the field of financial technologies (creation of a professional standard and evaluation tools).  Fig.5. Types of interaction between banks and fintech startups. Source: compiled by the authors. According to our opinion (see Figure 5), there are four main types of interaction between banks and fintech startups in Russia: the creation of accelerators, business incubators and hackathons; partnerships of various levels; participation in the authorized capital of fintech startups; cooperation within the ecosystem. It is also worth paying special attention to financial technologies that are created by commercial banks themselves. The creation of accelerators, business incubators and hackathons is the most initial form of interaction between banks and fintech startups, usually at this stage of cooperation fintech startups receive competence, knowledge and customer base from banks, and banks, in turn, at this stage can look closely, evaluate and make a decision about further cooperation [14]. It is worth noting that the creation of accelerators, business incubators and hackathons is a rather laborious and costly process, so only a small part of the participants can eventually receive the necessary investments for the development of their companies and become interesting to the organizers of accelerators and incubators. Partnerships of different levels are the second stage of interaction, at this stage banks can use fintech startups as counterparties to solve certain tasks within their businesses. The third stage of interaction between fintech startups and banks is the entry into the company's capital, at this stage, banks either become co-founders of startups by direct investment, create joint ventures, etc., or absorb and buy them out, turning them into their structural divisions. The fourth stage of cooperation between fintech startups and banks can be called cooperation within the ecosystem that the bank forms, this format of cooperation can be quite individual and depends primarily on the structure of the ecosystem that the bank itself forms. Thus, it follows from the above analysis that Russian banks are actively developing in the era of digitalization, becoming leaders in the introduction of innovative technologies into operations and forming large ecosystems with which millions of customers interact daily. Table 1. The level of introduction of financial technologies in banks by the example of members of the Fintech Association. |

bankAccelerators, business incubators, hackathons | Partnerships with fintech startups | Entering the capital of fintech startups | Creating your own fintech structures | Formation of ecosystems |

|

IndexSBERBANK PJSC | | + | | + | + | + | + |

5 | | PJSC VTB+ | | + | + | + | + | 5 | | JSC "Tinkoff Bank" |

+ | + | + | + | + | 5 | | GPB Bank JSC |

+ | + | +/- | +/- | + | 4 | | Alfa-Bank JSC+ | |

+ | +/- | +/- | +/- | 3,5 | | PJSC Bank "FC Otkritie"+ | | + |

+ | +/- | - | 3,5 | | Raiffeisenbank JSC+ | | +/- | +/- |

+/- | - | 2,5 | | JSC "Rosselkhoznadzor"+ | | +/- | +/- | +/- |

- | 2,5 | | PJSC "Ak Bars"+ | | +/- | +/- | +/- |

- | 2,5 | Source: compiled by the authors. To determine the level of development of financial technologies in the banking sector of the Russian economy, the authors analyzed the existing financial technology market, analyzed the structure of the Fintech Association. Next, a focus group of 9 banks of full members of the Fintech Association was identified and an analysis of their financial indicators was carried out, in particular, the amount of net assets and the total financial result for the periods 2020-2021, a content analysis at the macroeconomic level was carried out, an analysis of their development models was carried out using synthesis and comparison methods. The analysis was carried out on the basis of open sources: publications in the media, information on the official websites of banks, speeches by representatives of banks, etc. As part of the content analysis, the following factors were analyzed: creation of accelerators, business incubators, holding hackathons; partnerships with fintech startups; entry into the capital of fintech startups; creation of their own fintech structures; formation of ecosystems. If the factor satisfied the analysis conditions, then a "+" sign was put in the analysis table; if the factor did not satisfy the analysis conditions, then a "-" sign was put; in the case of an ambiguous situation or partial application, a "+/-" sign was put. The authors determined that, in accordance with the analysis in Table 1, if the index reaches 4.5-5, it can be argued that the bank from the analysis group is at a high level of development of financial technologies, with an index equal to 3.5-4, the bank from the focus group is at an average level of development of financial technologies, with an index equal to 3 and below the bank is at a low level of development of financial technologies. However, it is worth noting that the analysis was carried out only within the selected group of banks and the factors defined above (tools) and, accordingly, estimates of high, medium and low levels of financial technology development are not compared with other participants in the financial sector of the economy, which in turn may have an indicator/index, both higher and lower in depending on the selected group and tools. According to the analysis of Table 1, the highest level of introduction of financial technologies, according to the authors' calculations equal to the index 5, can be observed in three banks: Sberbank PJSC, VTB PJSC, Tinkoff Bank JSC. Sberbank PJSC has several accelerators within the framework of which support, expertise and evaluation of startups are carried out. Together with 500 Startups, which is one of the largest international business accelerators, Sberbank PJSC has the Sber500 accelerator, which has been operating since 2018.. Within the framework of the Sber500 accelerator, over the entire period of its existence, investments of more than 400 million rubles were attracted, half of the investments were made by Sberbank PJSC itself, the other half by the partners of the Sber500 accelerator; more than 100 contracts were concluded between the participants of the accelerator and Sberbank PJSC and more than 400 contracts between startups and partners of the Sber500 accelerator. Sberbank also has a corporate accelerator SberUp and a joint accelerator with the business incubator of the Higher School of Economics (HSE). In 2021, Sberbank PJSC, together with the Russian Venture Company (RVC), which is one of the structures of the RDIF, announced the creation of a fund for investments in startups with a volume of $ 100 million. Sberbank PJSC also has its own structures and significant shares in the following technology companies: SberMegaMarket (LLC "Marketplace"), Sberbank (LLC "Sound"), 2GIS (LLC "DoublGIS"), SberApteka (LLC "eApteka"), SberDevices (LLC "Sberdevices"), SberMarket (LLC "Instamart-Service"), Sberbank Mobile (Sberbank-Telecom LLC), Sberbank Logistics (Sberbank Logistics LLC), etc. All these companies are part of the Sberbank Group and, as part of the bank's strategy, are part of its ecosystem. The Bank has a structural subdivision of SberX, which is engaged in combining the above companies into an ecosystem. For the end user, access to the ecosystem is currently possible through any of the company's services, and to simplify this process, an SberID product (single sign-on to Sberbank and partners' services) and a subscription to the services of the SberPrime ecosystem have been created. PJSC VTB can also be called the largest player in the financial technology market. The Bank actively implements financial technologies in its activities both through cooperation with fintech startups and within its organizational structures. PJSC VTB has joint accelerators with the Skolkovo Foundation and the Internet Initiatives Development Fund (IIDF). As part of accelerators and business incubators, the bank allocates from 0.5 million rubles to 1.5 million rubles. for testing and piloting projects. PJSC VTB also has such structural divisions as: mobile operator VTB-Mobile, residential marketplace Metrkvadratny, subscription services for cars, bicycles, scooters, etc., as well as a number of joint projects with foreign IT and fintech companies, government agencies. The Bank has a stake in the capital of the IVI media company ( <url> LLC). It is worth noting that the bank is also working on the formation of a banking ecosystem, which within the framework of one company will provide services from various sectors of the economy, however, unlike its competitors, it is only at the initial level of ecosystem development.

JSC "Tinkoff Bank" forms accelerators and business incubators, in particular with its subsidiary CloudPayments, which was acquired in 2017-2019. In 2021, the bank acquired a service for storing cards and contactless payment "Wallet" (LLC "Contactless"). But unlike PJSC VTB and PJSC Sberbank, direct and venture investments of JSC Tinkoff Bank in startups are more targeted. This is primarily due to the fact that JSC Tinkoff Bank itself positions itself as a technology company and the necessary financial technologies are formed within the company. For example, the mobile operator Tinkoffmobile is a structural subdivision of the bank. The Bank also forms a banking ecosystem, which unites startups, as well as enterprises from different sectors of the economy. JSC "GPB Bank", JSC "Alfa-Bank" and PJSC Bank "FC Otkritie", in accordance with our analysis (Table 1), are at the average level of financial technology implementation, having received an index of 4, 3.5 and 3.5, respectively. JSC GPB Bank is a partner of the BankTech 3.0 accelerator program, organized by Fintech Lab LLC, as well as GreenTech Startup Booster 2021 of the Skolkovo Foundation. The Bank has a structural division of the mobile operator GPB-Mobile. In June 2021, the bank announced the development of the ecosystem through its subsidiary "Network of Partnerships" LLC, through the subscription "Fire" consumers get access to the products and services of ASNA (pharmacies), IVI (media company), Citylink (household appliances and electronics stores), Severgroup andGazprom". Thus, GPB Bank JSC is also actively developing an open-type ecosystem with a network of partners. Alfa-Bank JSC, together with its partners, conducts annual hackathons and accelerators, and fintech startups have the opportunity to directly offer their services to the bank through the website. In 2019, the bank began cooperation with fintech-stratap, engaged in data analysis, and providing personal financial assistant services, Rubbles. In 2021, the bank bought 100% of the service, a fintech startup, for non-cash payment of tips – netmonet. Unlike its competitors, Alfa-Bank JSC does not plan to create a banking ecosystem according to its development strategy, focusing more on financial services, creating financial super-services. It is worth noting that in 2019 the bank launched its own line of clothing and lifestyle products, and in 2021, together with X5 Group, launched the X5 Bank project, which suggests that perhaps the bank will not limit its activities to financial services only and some non-financial products and services will also be offered to consumers. PJSC Bank FC Otkritie, together with the Fintech Association and the Moscow Accelerator, conducts various kinds of webinars and hackathons, after which a number of participants are invited to take part in piloting their projects on the basis of the bank. PJSC Bank "FC Otkritie" owns 50% plus one share in the share of the bank of JSC "Tochka", which is a corporate bank and provides financial services only to legal entities and individual entrepreneurs, also recently JSC "Tochka" began to provide consulting and support services to sellers on the Ozon, Aliexpress, etc. marketplaces. thus, the bank will fully cover the needs of companies engaged in online trading. According to the authors' analysis (Table 1), Raiffeisenbank JSC, Rosselkhozbank JSC and Ak Bars PJSC are at a low level of financial technology implementation, having received each index equal to 2.5. All three banks periodically hold conferences, webinars, hackathons and, together with accelerator partners, in particular, the Skolkovo Foundation acts as a partner in conducting accelerators. Raiffeisenbank JSC issues an annual fintech atlas with an overview of the Russian and international fintech markets. JSC "Rosselkhozbank" in 2019 signed a memorandum with APIBank (LLC "Digital Banking Platforms") aimed at creating technological Open Banking solutions for JSC "Rosselkhozbank" on the basis of ARIVAPK for cooperation with fintech services, non-banking platforms and other fintech market participants. PJSC Ak Bars is also actively attracting fintech startups to cooperate and piloting their projects on its base. As can be seen from the analysis of Table 1, the level of introduction of financial technologies into the activities of commercial banks directly affects the transformation of their business models, and, in particular, the high level of introduction of financial technologies on the formation of ecosystems by banks. In accordance with the analysis, the formation of ecosystems is primarily carried out by the largest banks in terms of net assets and financial results, since this process is highly expensive and high-tech, in which it is necessary to involve almost all structural divisions of the bank. As can be seen from Table 1 and from the analysis of the results, the introduction of financial technologies into the activities of commercial banks is an essential condition for further development, with the preservation and acceleration of growth rates, of the largest banks in Russia and the formation of banking ecosystems. As a rule, fintech startups focus on developing in freer financial niches with high margins, using new flexible and effective methods and mechanisms of activity [5]. Fintech startups do not have the legal capacity to open and maintain accounts of their clients and perform a number of other operations, thus they are interested in cooperation with banks and other traditional financial market participants [18]. In this case, fintech startups and traditional financial companies can act as complementary parts of the same business structure [7]. Some researchers such as J. Coughlin, P. Vigna, J. Rickards, M. Swan, J. Barberis are of the opinion that the rapid development of the fintech industry in the world will eventually have an impact on the extinction of the banking sector of the economy in the medium and long term, and in the short term at least fintech startups will push banks in the financial sector of the economy. However, given the conditions prevailing in the Russian market, we are of the opinion that the financial technology industry in Russia will develop not in competition with credit institutions, but within the framework of cooperation and within commercial banks.

It is worth noting that, classifying fintech startups from the point of view of banks, they can be divided into three main types: client-oriented fintech startup (startup competitor), supporting fintech startup (startup employee) and mixed [8]. The cooperation of fintech startups with banks also has advantages for fintech companies themselves. Partnerships with banks allow fintech startups to solve a number of regulatory problems that arise in the course of their activities, companies get access to the customer base of banks and its infrastructure and in some cases can also count on affiliation with the brand of a large bank [3]. Conclusion. The further digitalization of banks, the development of financial technologies in the banking sector of the economy, the development of fintech startups and their subsequent cooperation with banks is becoming an obvious fact. It is worth noting that the transformation of the financial sector of the economy, where fintech-strataps largely compete with traditional credit institutions and affect the transformation of the overall landscape of the financial sector in Russia is unlikely. Unlike foreign financial markets, where there is a high level of development of individual independent fintech startups, in Russia there is a situation where a significant part of financial technologies are developed within the banks themselves, and fintech startups either cooperate at all levels with banks, or eventually are bought out by banks becoming their structural divisions. The level of interaction between fintech startups in this case, in particular, depends on which bank the fintech startups cooperate with. As a result, one can observe a clear preference for such major players as Sberbank PJSC, VTB PJSC, Tinkoff Bank JSC, etc. to the formation of financial technologies within their companies and the creation of banking ecosystems by creating a network of financially dependent enterprises. While medium and small banks, including Alfa-Bank JSC, Raiffeisenbank JSC, Ak Bars PJSC, etc. they give preference to the partner type of interactions.

References

1. Alt R., Beck R., Smits M.T. FinTech and the transformation of the financial industry // Electronic Markets. 2018. Vol. 28.

2. Aliev M.M., Mamedov M.A., Rzayeva V.V., Safarli A.Kh. Ecosystem as a new model for the development of financial organizations // Humanities, socio-economic and social sciences // M. №8-2021, https://doi.org/10.23672/m6478-2891-3501-e .

3. Klioutchnikov I., Sigova M., Beizerov N. Chaos Theory in Finance // Procedia Computer Science Volume 119, 2017, P. 368-375. https://doi.org/10.1016/j.procs.2017.11.196 .

4. Bouwman, H., den Hooff, V., van de Wijngaert, L., & van Dijk, J. (2005). Information and communication technology in organizations: Adoption, implementation, use and effects. Sage Publications. https://doi.org/10.4135/9781446211519 .

5. Banking beyond banks and money: A guide to banking services in the 21 century / Ed. P. Tasca, T. Aste, L. Pelizzon, N. Perony. N.Y.: Springer, 2016. https://doi.org/10.1007/978-3-319-42448-4 .

6. Gimpel H., Rau D., Roglinger M. Understanding FinTech start-ups-a taxonomy of consumer-oriented service offerings // Electronic Markets. 2018. Vol. 28. Issue 3. P. 245-264. https://doi.org/10.1007/s12525-017-0275-0 .

7. Haddad C., Hornuf L. The emergence of the global fintech market: Economic and technological determinants // Small business economics. 2018. P. 13.

8. Kang J. Mobile payments in Fintech environment: Trends, security challenges, and services // Human-centric Computing and Information sciences. 2018. Vol. 8. Issue 1. P. 14.

9. Kleiner G.B., Rybachuk M.A., Karpinskaya V.A. (2020). Development of ecosystems in the financial sector of Russia // Manager. Vol. 11, No. 4, pp. 2–15. https://doi.org/10.29141/2218-5003-2020-11-4-1 .

10. Kotlyarov I. D. Fintech: essence and implementation models // ECO. 2018.No 12 (534). https://doi.org/10.30680/ЕСО0131-7652-2018-12-23-39 .

11. Lee I., Shin Y.J. (2018). Fintech: Ecosystem, business models, investment decisions, and challenges. Business Horizons, vol. 61, no. 1, pp. 35–46. https://doi.org/10.1016/j.bushor.2017.09.003

12. Levitskaya E.N., Shashkina E.O. Prospective directions of interaction between the banking business and fintech startups // Problems of the national strategy. 2020. No 1 (58).

13. Maslennikov V.V., Fedotova M.A., Sorokin A.N. New financial technologies change our world. Finance: Theory and Practice. 2017;21(2):6-11. (In Russ.) https://dфoi.org/10.26794/2587-5671-2017-21-2-6-11 .

14. Zhdanova O.A. Fintech accelerators-institutions of the fintech ecosystem // Society: Politics, Economics, Law. 2018.No 4. https://doi.org/10.24158/pep.2018.4.6.

15. Zhu K., Kraemer K. L., Xu S., Dedrick J., (2004). Information technology payoff in E-business environments: An international perspective on value creation of E-business in the financial services industry. Journal of Management Information Systems, 21 (1), 17-54. https://doi.org/10.1080/07421222.2004.11045797 .

16. Schueffel P. (2016). Taming the beast: A scientific definition of fintech. Journal of Innovation Management, vol. 4, no. 4, pp. 32–54. https://doi.org/10.24840/2183-0606_004.004_0004.

17. Competition in the digital age. Strategic challenges for the Russian Federation. The World Bank. 2018. Electronic resource. URL: http://documents.worldbank.org/curated/en/848071539115489168/pdf/Competing-in-the-Digital-Age-Policy-Implications-for-the-Russian-Federation-Russia-Digital-Economy-Report.pdf . (date of access: 10/25/2021).

18. Fintech and the evolving landscape // Accenture. 2016. P. 5. URL: https: // www.accenture.com/_acnmedia/pdf-15/accenture-fintech-evolving-landscape.pdf (date accessed: 01.10.2021).

19. Fintech Services Penetration Index-2019. Ernst & Young. 2019. Electronic resource. URL: https://www.ey.com/Publication/vwLUAssets/ey-fai-2019-rus/$FILE/ey-fai-2019-rus.pdf . (date of access: date of access: 10/25/2021)

20. Global FinTech Outlook March 2016 // Blurring Borders: How FinTech Companies Are Influencing the Financial Services Sector. Electronic resource. URL: https://www.pwc.ru/ru/banking/publications/fintech-global-report-rus.pdf (date accessed: 09/10/2021).

21. Sedykh I.A., Market of innovative financial technologies and services, Moscow: Higher School of Economics, Development Center, 2019. Electronic resource. URL:https://dcenter.hse.ru/data/2019/12/11/1524406294/Рынок%20финансовых%20технологий-2019.pdf (date of access: 10/25/2021).

Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The article submitted for review reflects the results of the authors' analysis of the impact of financial technologies on the banking sector of the Russian economy. The research methodology is based on the application of such methods of scientific research as analysis, synthesis, ascent from the abstract to the concrete, logical and historical method, other general scientific methods, as well as the analysis of statistical economic data. The authors rightly attribute the relevance of the study to the fact that in the context of digitalization of the financial sector of the economy, the introduction of innovative technologies into the activities of financial organizations becomes an economic necessity and is carried out both through the creation of such technologies directly within the banks themselves and through cooperation with existing companies providing financial technologies. The scientific novelty of the reviewed study, according to the reviewer, lies in the presented results of the analysis of the impact of financial technologies on the modern banking sector of the Russian economy, with the differentiation of the features of digital transformations in large, medium and small banks. The following sections are structurally highlighted in the article: Introduction, Literature review, Analysis of the fintech market in Russia, the impact of fintech on the activities of commercial banks, Conclusion and Bibliography. The introduction substantiates the relevance of the study, reflects the object and methods of the study, the source materials for its implementation. The following is a review of the literature on the topic under consideration, as a result of summarizing the published works, the authors decided to adhere to an approach to determining where fintech is a set of innovative technologies in the financial sector of the economy based on the use of innovative and digital means of communication and data processing, transforming both the business models of traditional organizations in the financial market and the interaction between participants the market. The analysis of the fintech market in our country reflects the results of visualization of data on the volume of fintech transactions in Russia in the period from 2017 to 2021 by segments: electronic payments, non-banking, personal finance; on the number of non-banking users and the degree of penetration of online banking in Russia in 2010-2021; on the revenue of leading fintech companies Russia in 2020 When considering the impact of fintech on the activities of commercial banks, a systematization of the types of interaction between banks and fintech startups was carried out, the level of implementation of financial technologies in banks was analyzed using the example of members of the Fintech Association. In conclusion, the authors note a distinctive feature of the transformation of the domestic financial sector of the economy – in Russia, a significant part of financial technologies are developed within the banks themselves, and fintech startups either cooperate at all levels with banks, or eventually are bought out by banks becoming their structural divisions. The bibliographic list includes 21 sources – publications of domestic and foreign authors in scientific journals, as well as online resources on the topic of the article. The text contains targeted references to literary sources confirming the existence of an appeal to opponents. The reviewed material corresponds to the direction of the journal "Finance and Management", has been prepared on an urgent topic, contains theoretical justifications, elements of scientific novelty and practical significance and is recommended for publication.

Link to this article

You can simply select and copy link from below text field.

|

|